by

by Introduction:

In the dynamic landscape of business, entrepreneurs are increasingly recognizing the importance of embracing digital solutions for accounting. E-accounting not only streamlines financial processes but also provides valuable insights that can shape strategic decision-making. For those venturing into the world of entrepreneurship, adopting effective e-accounting practices is crucial. In this blog, we will explore five indispensable e-accounting tips tailored specifically for budding entrepreneurs.

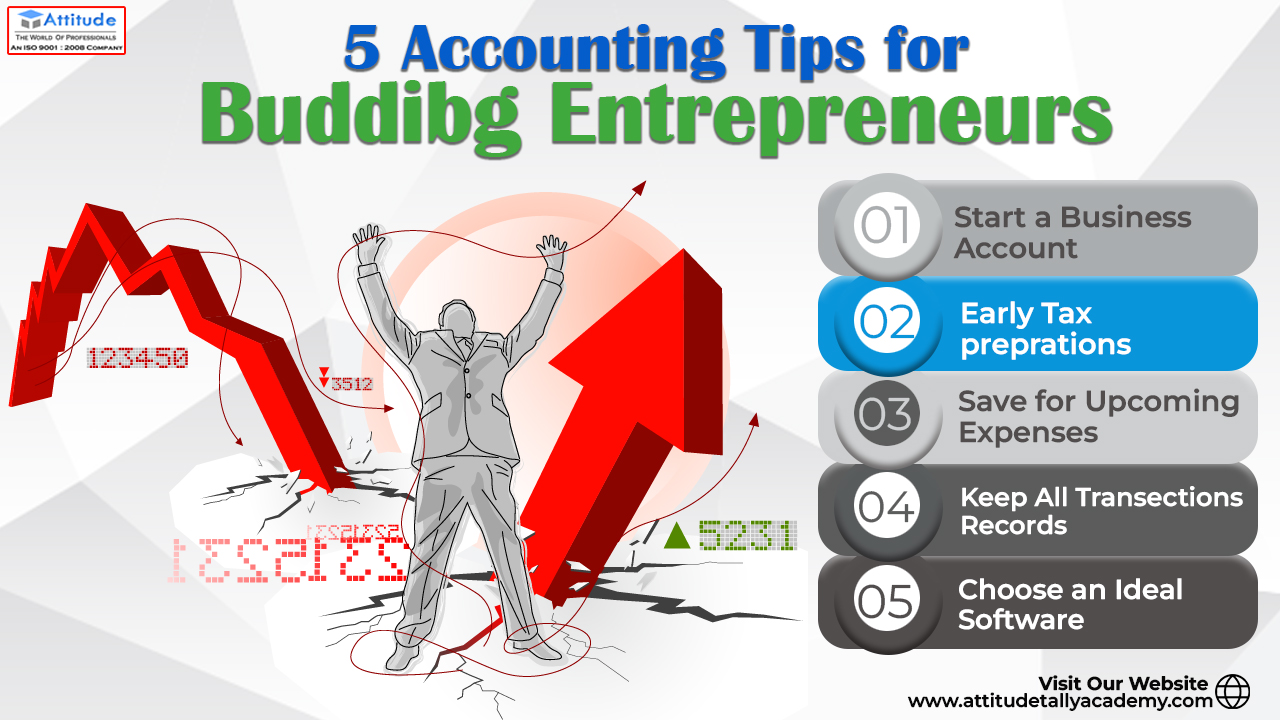

Start a Business Account:

One of the fundamental steps for any entrepreneur is to establish a dedicated business account. This separation of personal and business finances is pivotal for maintaining financial clarity. By having a distinct business account, you not only create a professional image but also simplify your bookkeeping processes. This separation lays the foundation for organized financial management, a cornerstone for the success of any business.

Early Tax Preparations:

Tax obligations are a reality for every business, and proactive tax planning can significantly impact your bottom line. Start early by understanding your tax liabilities and preparing for them throughout the year. Early tax preparations not only help in avoiding last-minute stress but also enable you to identify potential deductions and credits, maximizing your tax efficiency. Seek professional advice if needed to ensure compliance with tax regulations.

Save for Upcoming Expenses:

Entrepreneurs often face unexpected expenses, from equipment repairs to sudden marketing opportunities. Setting aside funds for these unforeseen costs is a prudent strategy. Create a budget that includes a contingency fund for unexpected expenses. This financial cushion can prevent your business from facing financial strain during challenging times, allowing for smoother operations and growth.

Keep All Transaction Records:

Accurate record-keeping is the backbone of effective e-accounting. Keep detailed records of all your financial transactions, including income, expenses, and receipts. This not only facilitates seamless tax filings but also provides a comprehensive overview of your business’s financial health. Utilize accounting software to automate the process, ensuring accuracy and saving valuable time that can be redirected towards business growth.

Choose an Ideal Software:

Selecting the right accounting software is a pivotal decision for entrepreneurs embracing e-accounting. Consider your business needs, scalability, and user-friendliness when choosing accounting software. Look for features such as invoicing, expense tracking, and financial reporting. Cloud-based solutions offer accessibility from anywhere, promoting flexibility in managing your finances. Popular choices include QuickBooks, Xero, and FreshBooks.

Conclusion:

In conclusion, the adoption of e-accounting practices is a strategic move for budding entrepreneurs aiming for sustainable growth. Start by establishing a dedicated business account, engage in early tax preparations, save for upcoming expenses, maintain meticulous transaction records, and choose an ideal accounting software. By incorporating these tips into your financial management strategy, you pave the way for a more organized, efficient, and successful entrepreneurial journey.

Suggested Link: